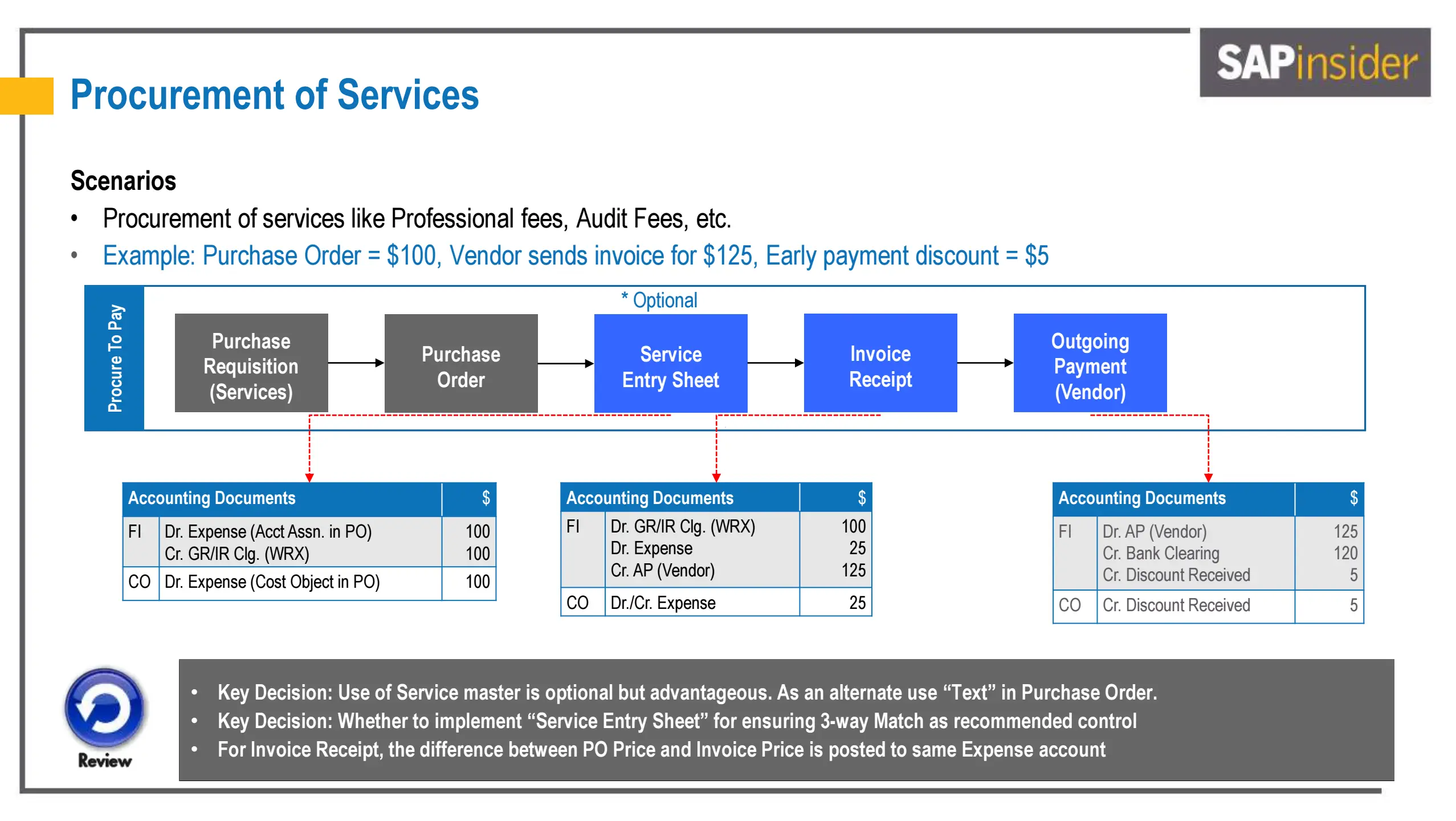

Services procurement in SAP ERP, unlike materials procurement, deals with acquiring intangible services such as professional fees, audit fees, or consulting. While the process shares similarities with materials procurement, the accounting implications and journal entries have their own nuances. Let’s break down a typical services procurement flow and examine the journal entries at each key stage, referencing the visual provided in this post.

The Services Procurement Flow (and Accounting Touchpoints)

The standard flow for services procurement in SAP generally follows these steps:

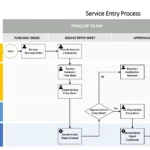

1. Purchase Requisition (Services):

The process begins with a department identifying the need for a service and creating a Purchase Requisition. At this stage, typically no journal entries are created. It’s an internal request, not a legally binding transaction yet.

2. Purchase Order (PO):

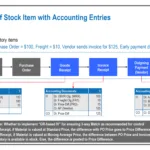

Based on the requisition, a Purchase Order is created and sent to the vendor. This document outlines the service to be provided, agreed-upon price, and terms. Let’s use the example from the image: Purchase Order = $100.

Journal Entry Impact at Purchase Order Creation (FI & CO):

FI (Financial Accounting):

| Account | Debit | Credit |

|---|---|---|

| Expense (Based on Account Assignment in PO) | $100 | |

| GR/IR Clearing Account (WRX) | $100 |

CO (Controlling):

| Account | Debit | Credit |

|---|---|---|

| Expense (Cost Object in PO) | $100 |

Explanation:

- Debit to Expense: We recognize an expense commitment as soon as the Purchase Order is approved. The specific expense account is determined by the account assignment details specified in the Purchase Order (e.g., consulting expense, audit fees expense).

- Credit to GR/IR Clearing (WRX): “GR/IR” stands for Goods Receipt/Invoice Receipt clearing. While we don’t have a physical “goods receipt” for services, the GR/IR clearing account acts as an interim account. It temporarily holds the liability until the service is confirmed and the invoice is received. “WRX” often denotes a GR/IR clearing account specific to goods and service receipts.

- CO Posting: In Controlling (Management Accounting), a corresponding expense is also recorded against the relevant cost object (e.g., cost center, project) defined in the Purchase Order. This ensures cost allocation for internal reporting and analysis.

3. Service Entry Sheet (Optional but Recommended):

This step is crucial for service procurement control. After the service is performed, a “Service Entry Sheet” is created to confirm the completion and acceptance of the service quantity and quality. While the visual indicates it’s optional, implementing a Service Entry Sheet is strongly recommended for 3-way matching (PO, Service Entry Sheet, Invoice) and better control.

No direct journal entries are typically triggered solely by the Service Entry Sheet in standard configurations. The Service Entry Sheet primarily acts as an approval mechanism and a prerequisite for invoice verification. However, in some more complex scenarios, a preliminary accrual might be posted based on Service Entry Sheet approval before the invoice arrives, but for simplicity, we’ll follow the visual’s depiction where the next accounting event is at Invoice Receipt.

4. Invoice Receipt:

The vendor sends an invoice for the services rendered. In our example, the Vendor sends an Invoice for $125. This is a difference of $25 from the PO amount of $100.

Journal Entry Impact at Invoice Receipt (FI & CO):

FI (Financial Accounting):

| Account | Debit | Credit |

|---|---|---|

| GR/IR Clearing Account (WRX) | $100 | |

| Expense | $25 | |

| Accounts Payable (Vendor) | $125 |

CO (Controlling):

| Account | Debit | Credit |

|---|---|---|

| Dr./Cr. Expense | $25 |

Explanation:

- Debit to GR/IR Clearing (WRX): We clear out the initial $100 credit balance we established in the GR/IR clearing account at the Purchase Order stage. This signifies that the service has been delivered and invoiced.

- Debit to Expense: Since the invoice amount ($125) is higher than the Purchase Order amount ($100), we need to recognize the additional $25 expense. This is posted to the same expense account used earlier, ensuring the total expense reflects the actual invoice value. Note: If the invoice was lower than the PO, we would credit the expense account to reduce it.

- Credit to Accounts Payable (Vendor): We record the liability to the vendor for the invoice amount of $125. This represents the amount we owe to the vendor.

- CO Posting: The $25 difference is also reflected in Controlling, updating the expense against the cost object to match the actual invoiced amount.

5. Outgoing Payment (Vendor):

Finally, the payment is made to the vendor. In our example, an Early Payment Discount = $5 is received.

Journal Entry Impact at Outgoing Payment (FI & CO):

FI (Financial Accounting):

| Account | Debit | Credit |

|---|---|---|

| Accounts Payable (Vendor) | $125 | |

| Bank Clearing Account | $120 | |

| Discount Received | $5 |

CO (Controlling):

| Account | Debit | Credit |

|---|---|---|

| Discount Received | $5 |

Explanation:

- Debit to Accounts Payable (Vendor): We reduce the liability to the vendor by $125, as we are making the payment.

- Credit to Bank Clearing Account: This reflects the outflow of cash from our bank account. A “Bank Clearing Account” is often used for reconciliation purposes before hitting the main bank account.

- Credit to Discount Received: The early payment discount of $5 reduces our overall expense. “Discount Received” is typically an income account or a contra-expense account, effectively lowering the total expense recognized for the service.

- CO Posting: The discount received is also reflected in Controlling, reducing the cost allocated to the cost object.

Key Takeaways & Considerations:

- Service Master (Optional but Advantageous): While not explicitly shown in the journal entries, using a Service Master can streamline the process and ensure consistent descriptions and pricing for frequently procured services.

- Service Entry Sheet Importance: Implementing a Service Entry Sheet adds a crucial layer of control and enables a robust 3-way match (PO-Service Entry Sheet-Invoice), especially for complex or high-value services.

- Invoice Price Differences: As demonstrated in the example, differences between the PO price and Invoice price are adjusted directly to the Expense account at the time of invoice receipt. This ensures accurate expense recognition and reflects the actual cost incurred.

- GR/IR Clearing Account: Understanding the role of the GR/IR clearing account is fundamental in services procurement accounting. It bridges the gap between PO creation and Invoice receipt, ensuring accurate accruals and liability tracking.

By understanding these journal entries, businesses can gain better insights into the financial impact of their services procurement activities, ensure accurate financial reporting, and maintain robust internal controls. This technical overview should provide a solid foundation for navigating the accounting aspects of services procurement.